CoStar News: US office leasing holds steady at midyear

Raleigh-Durham is seeing the same national trend: tenants are active, but many are favoring smaller, higher-quality spaces in strong submarkets like RTP/I-40, Downtown Raleigh, Downtown Durham, and amenity-rich mixed-use areas.

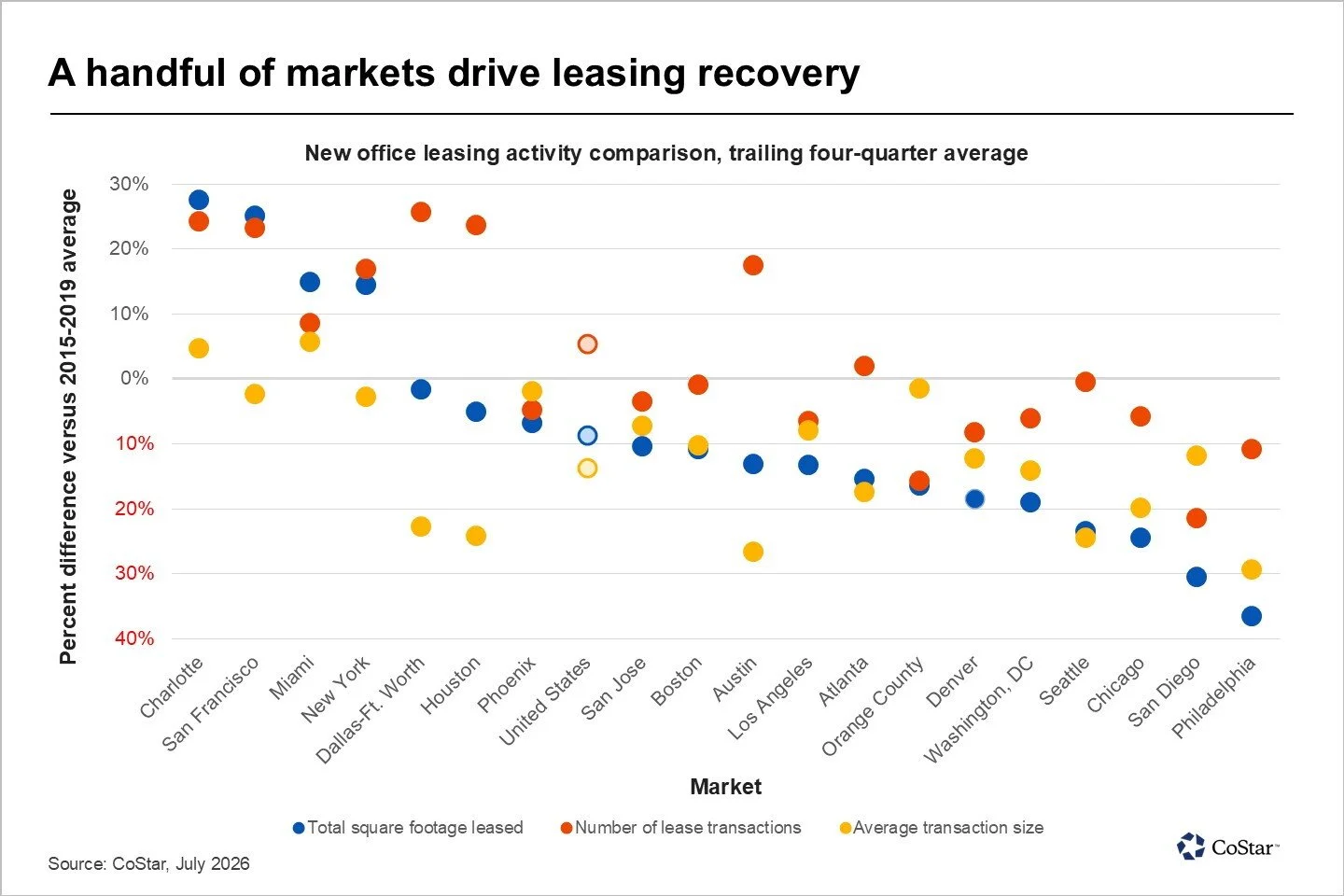

While demand remains strong, smaller deal sizes suppress volume in most markets:

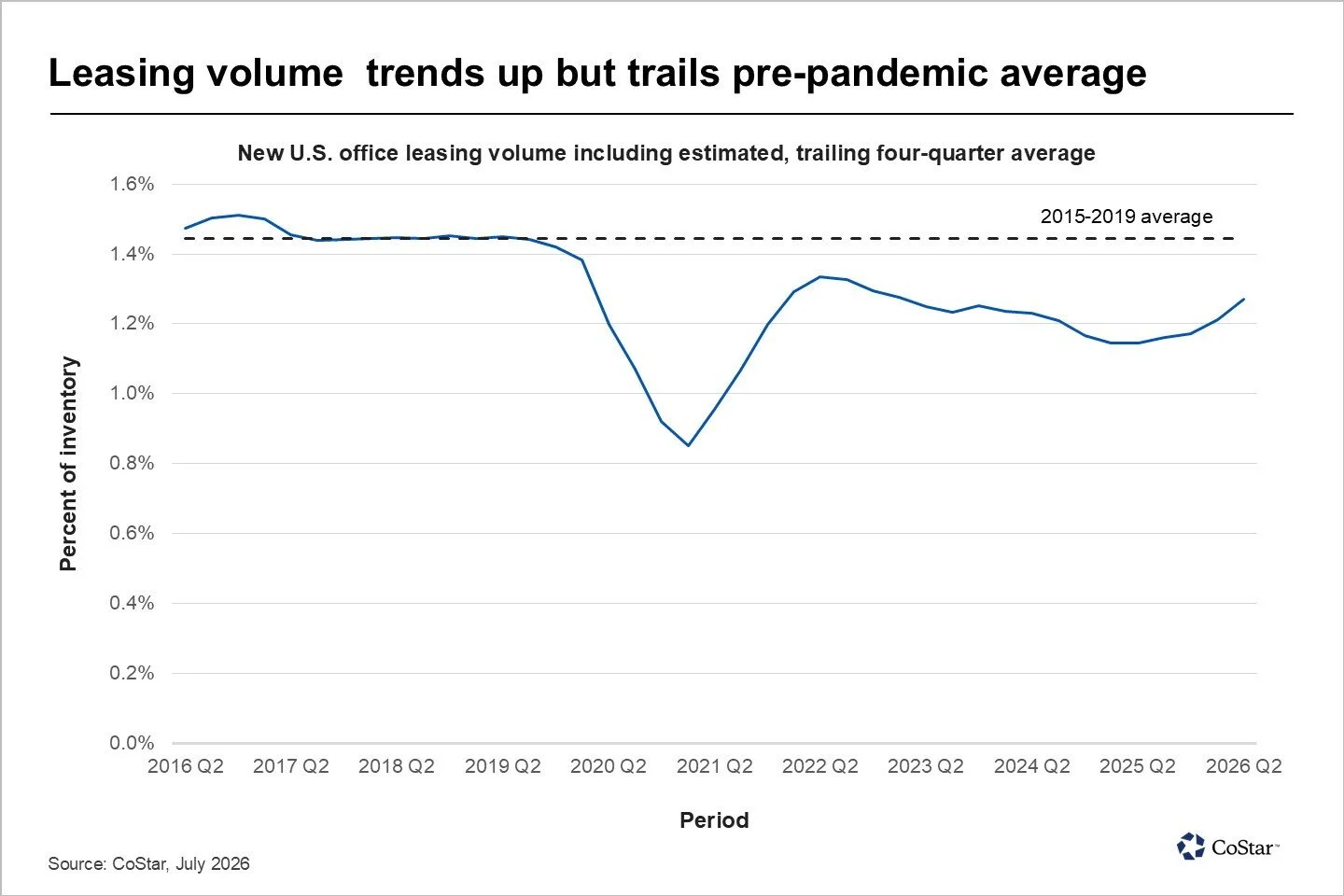

Office tenants signed new leases for an estimated 115 million square feet during the second quarter of 2026, roughly in line with revised first-quarter numbers but still slightly below the quarterly average from 2015 to 2019.

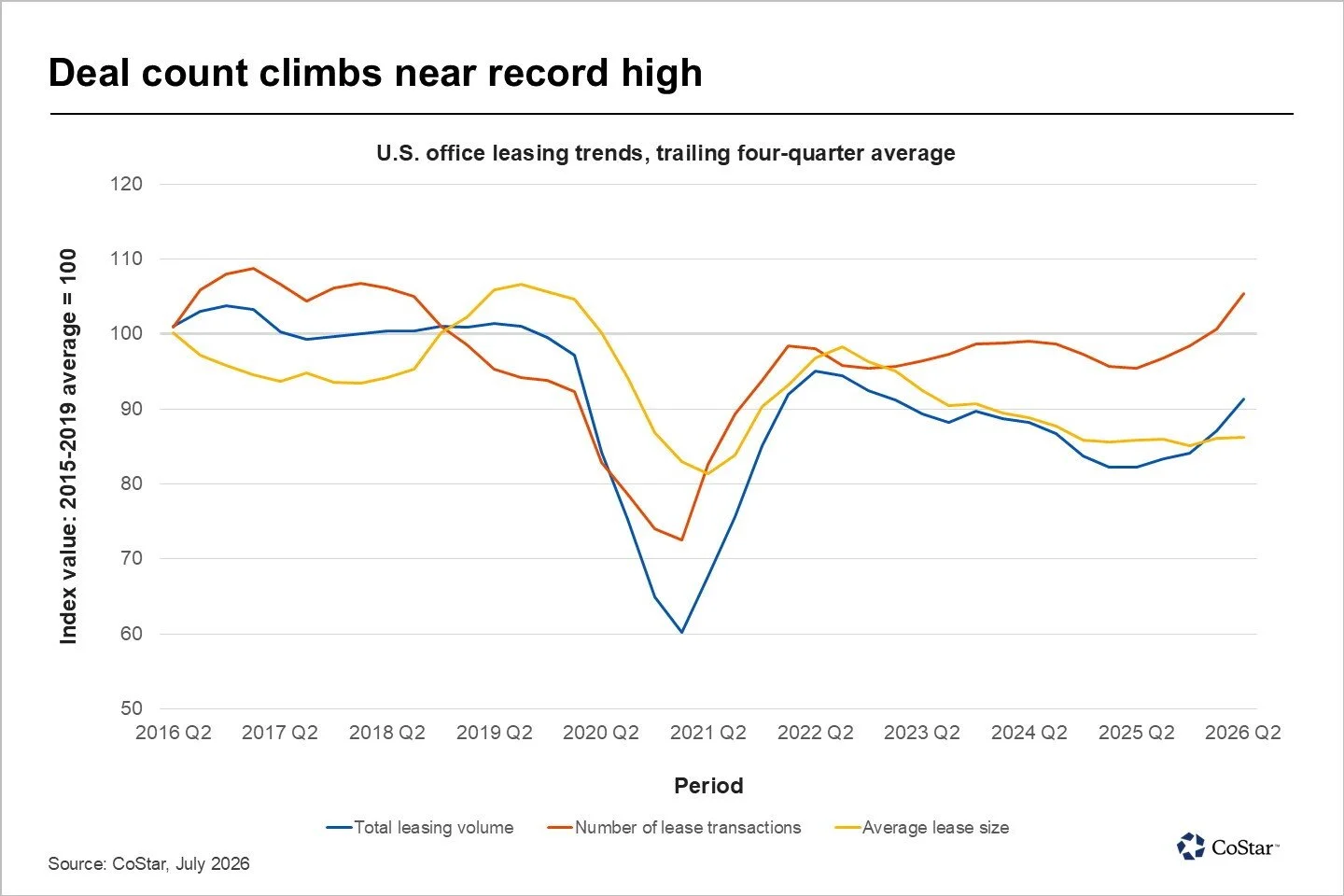

Since the middle of 2025, office leasing volume has climbed to within roughly 9% of the pre-pandemic norm for a 12-month period. Market vibrancy has made more than a full recovery, with the number of office lease transactions near the all-time high. However, the amount of space leased in a typical deal has settled about 15% below its historical norm, a level that has held steady for two years.

These findings are based on collected and estimated data from office leases executed through the end of the second quarter. As with previously reported leasing data, only new lease commitments are considered. Renewals, which tend to have little impact on overall occupancy, are excluded from this analysis.

The results suggest a market that is demonstrating a sustained recovery but is also bending to constraints imposed by supply and demand. Hiring has been slow and is expected to remain so, especially in traditional knowledge-oriented industries.

Despite this, organizations in some sectors have been actively committing to new space. Among them are financial service institutions, many of which have firmer expectations for frequent office attendance.

Alongside these big banks are a growing number of venture-backed technology companies, including those focused on artificial intelligence, that are seeking out space in anticipation of hiring. Some of these AI firms have joined the group of relatively small professional services firms in a trend of taking small spaces in highly desirable locations.

The distribution of occupiers signing new leases is skewed toward these smaller tenants, resulting in a smaller average deal size. Part of this, however, is because relocation options for the largest office occupiers are vanishing. With new construction activity constrained at a historically low level, few contiguous blocks of premium space remain available in major markets. This, in turn, is keeping overall leasing volume below its customary pre-2020 level despite a sustained surge in activity.

A few markets are bucking the small-lease trend, including such finance-heavy locations as Charlotte, North Carolina, Miami and New York. In San Francisco, office lease sizes have also returned to their historical average as the largest AI-oriented firms have become hungry for space. As a result, office leasing volume is well above its long-run average in all four markets.

The Dallas and Houston office markets have also seen overall leasing volume remain close to their pre-pandemic averages, with activity rising enough to offset the trend toward smaller deals. Elsewhere, though, leasing volume remains depressed, with deal counts struggling to recover in about half of the country’s 20 largest office markets.

Second-quarter new leasing performance, while roughly on par with a strong first quarter, could indicate a de facto ceiling on volume for the current cycle. High churn could help maintain office leasing volume near its current level. Smaller leases often have shorter terms, which can catalyze faster, higher deal flow that could keep volume steady as tenants sort themselves into and out of existing spaces.

On the other hand, the lack of relocation options is expected to force many large occupiers to renew in place, clogging up the market that would typically emerge to backfill their current spaces. This, coupled with near-stagnant growth in knowledge-industry jobs, suggests that office leasing volume is likely to decelerate in the quarters ahead.

-

Article Provided By: Phil Mobley, CoStar Analytics

What does these mean for the Raleigh-Durham market?

What this means for the Triangle is that office demand is recovering, but in a more selective and right-sized way. Raleigh-Durham is seeing the same national trend: tenants are active, but many are favoring smaller, higher-quality spaces in strong submarkets like RTP/I-40, Downtown Raleigh, Downtown Durham, and amenity-rich mixed-use areas. With Q1 2026 Triangle office leasing over 503,000 SF and vacancy improving in some reports, the market appears to be stabilizing rather than broadly rebounding. For landlords, the opportunity is strongest in well-located, move-in-ready Class A or boutique office space; for tenants, the window remains favorable, but the best blocks of quality space may become harder to find as activity continues.

Need help navigating the Triangle office market?

Whether you're searching for office space, marketing a property, renewing a lease, or evaluating an investment, SVN | Real Estate Associates provides local expertise backed by national resources. Reach out to our team to discuss your goals or request a customized market analysis tailored to your business or portfolio.